When you see an option price (premium) like ₹150 for a NIFTY call, have you wondered how that number is decided? Option premiums consist of two parts: intrinsic value and extrinsic value (also known as time value). Understanding these will demystify why some options are cheap and some are expensive.

Intrinsic Value:

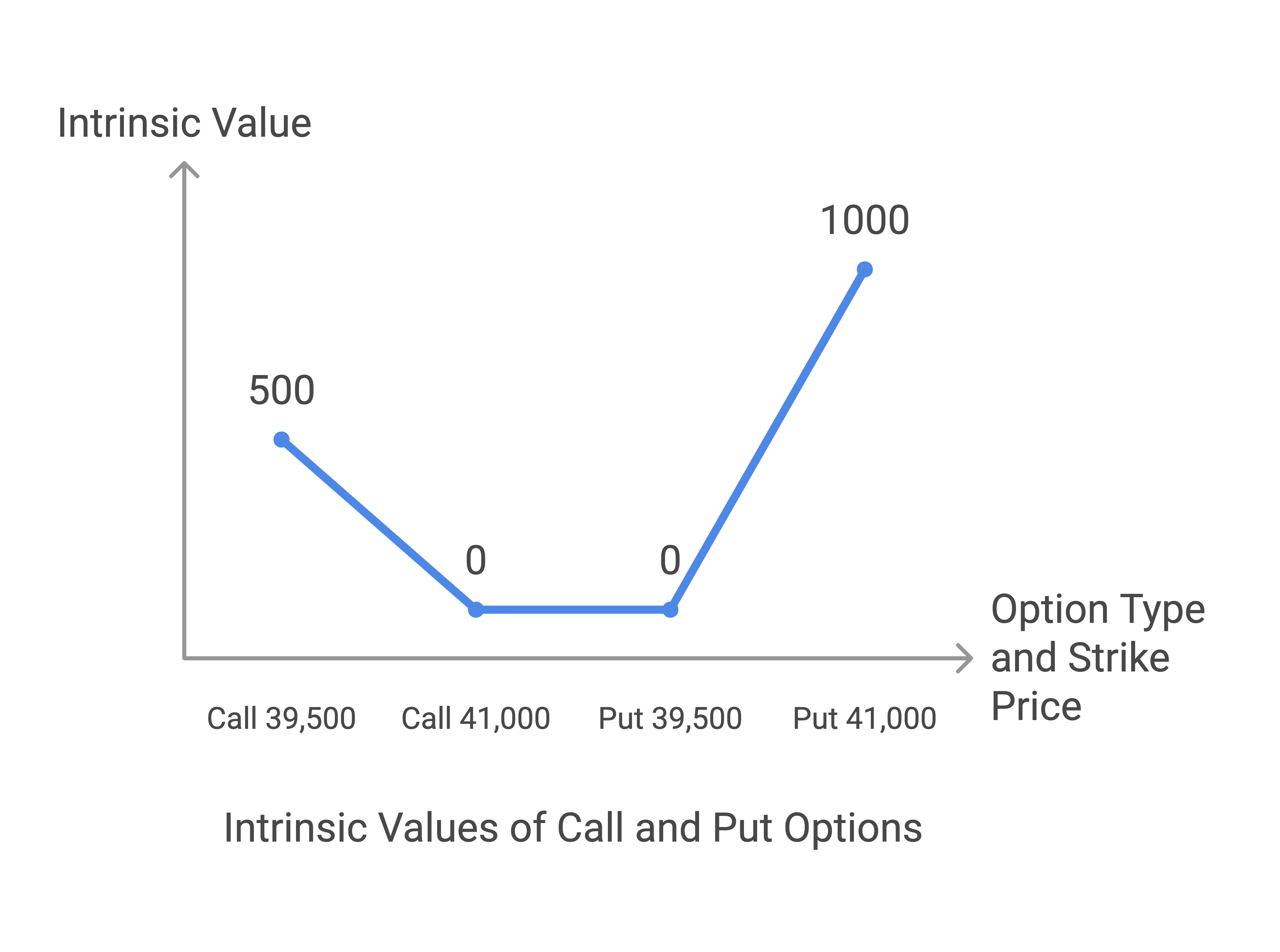

This is the real, tangible value of an option if it were exercised right now. It reflects how far in-the-money an option is (more on moneyness soon). For a call option, intrinsic value = max(0, current underlying price – strike price). In other words, if the underlying (spot price) is above the strike, the difference is intrinsic value (because you could buy at strike and immediately sell at market for a profit). If the underlying is below the strike, intrinsic value is 0 (a call can’t have negative intrinsic – you wouldn’t exercise it). For a put option, intrinsic = max(0, strike – current price) (a put has intrinsic value if the strike is above the current market price, meaning you can sell higher than market). Example: If BANKNIFTY is at 40,000:

A 39,500 strike call has intrinsic value of 40,000 – 39,500 = 500 points.

A 41,000 strike call has intrinsic value 0 (it’s not in-the-money).

A 39,500 strike put has intrinsic 0 (because you wouldn’t sell lower than market).

A 41,000 strike put has intrinsic value of 41,000 – 40,000 = 1,000 points.

Intrinsic value can never be negative – it’s either zero or some positive amount, depending on the option being ITM or not (Moneyness of an Option Contract – Varsity by Zerodha). It’s essentially the immediate exercise value.

Extrinsic Value (Time Value):

This is any extra premium above intrinsic value. It captures all additional value from factors like time left to expiry and volatility. Even if an option is out-of-the-money (no intrinsic value), it can still cost something because there’s a chance it could become valuable before expiry. Extrinsic value = Option Premium – Intrinsic Value. It represents the “hope” or probability that by expiry the option will move into profit. Key components influencing extrinsic value:

Time to Expiry: More time = higher extrinsic value (because there’s a longer chance for the underlying to move and make the option profitable). An option with 30 days to expiry will have more time value than one with 3 days to expiry, all else equal.

Volatility: Higher expected volatility = higher extrinsic value. If the underlying swings a lot, even far OTM options have a chance to become ITM, so they command a higher premium. We’ll dive deeper into volatility later.

Interest Rates & Dividends: Minor factors for extrinsic value (they influence option pricing models slightly – interest rates via cost-of-carry and expected dividends can lower calls’ extrinsic a bit).

Time Decay (Theta):

Extrinsic value erodes as time passes. This makes sense – the less time remains, the fewer chances for the underlying to move in your favor. This erosion of premium as days pass is called time decay, measured by the Greek letter Theta (we’ll cover Greeks in depth soon). For now, know that if you buy an option, time is working against you – every day, a bit of that extrinsic value ticks away (especially as expiry nears). If you sell an option, time decay works in your favor (you want the premium to decay).

Real-World Premium Breakdown:

Let’s break down a real example. Suppose NIFTY is at 18,000 with one week to expiry:

The 18,000 Call (ATM) is trading at ₹120. If ATM, it has roughly 0 intrinsic (since strike = spot, assume at-the-money intrinsic is zero or near-zero). So the entire ₹120 is extrinsic value (time value + volatility premium).

The 17,500 Call (deep ITM) is trading at ₹520. Now, intrinsic value here = 18,000 – 17,500 = ₹500. So out of ₹520 premium, ₹500 is intrinsic and only ₹20 is extrinsic (because it’s deep in the money and almost certain to expire in profit, but still has a little time value).

The 18,500 Call (OTM) is trading at ₹10. It has 0 intrinsic (since 18,500 is above current NIFTY). The ₹10 is pure extrinsic, reflecting a small chance that NIFTY might rally above 18,500 in a week. If it doesn’t, this ₹10 will decay to 0 by expiry.

As you see, ATM options have the most extrinsic value (they have the highest time value because they are at the point of uncertainty), ITM options are mostly intrinsic value (already in profit, so price mainly reflects that intrinsic), and OTM options are purely extrinsic (all hope, no intrinsic). In fact, ITM options are always more expensive than OTM options in absolute premium because they include intrinsic value. But in terms of extrinsic, ATM is king.

To summarise:

Option Premium = Intrinsic Value + Extrinsic Value.

Intrinsic value is immediate exercise value (only for ITM options).

Extrinsic value is everything else (time + volatility value) and decays as expiry approaches.

As an option buyer, you pay both values; as a seller, you receive them, and hope to keep as much extrinsic as possible by expiry.

Now that we know what makes up the premium, let’s classify options by their relationship to the current price – that is, moneyness.