Before you dive into options trading, it's vital to understand how much money you need to put up for various option positions, and the regulations set by SEBI (Securities and Exchange Board of India) regarding margins. Margin is basically the collateral or money you must have in your account to cover potential losses, especially when you are short (selling) options. We'll explore the margin requirements for different scenarios (buying vs selling, hedged vs naked), and talk about recent regulatory changes in India that affect traders.

Buying Options – Premium Only:

The simplest case: if you buy a call or put, you do not need to post any margin. You just pay the full premium upfront. The premium itself is your maximum loss. For example, if you buy 2 lots of Nifty 18,000 Call at ₹100 premium, and Nifty’s lot is 50, you pay ₹100 * 50 * 2 = ₹10,000. That's it. No other margin. Your loss is capped at ₹10k (if it expires worthless), and gains theoretically unlimited for calls (or up to nearly strike for puts). This is why option buying is accessible even for small accounts – you know exactly how much you’re risking, and you pay it upfront.

Selling (Writing) Options – Margin Required:

When you sell an option, you are taking on potentially large risk (e.g., if you sell a naked call, the market could skyrocket, incurring huge loss). The exchange requires you to put up margin for this. The margin for selling an option is similar to margin for a futures position because a short option can become like a futures exposure if ITM.

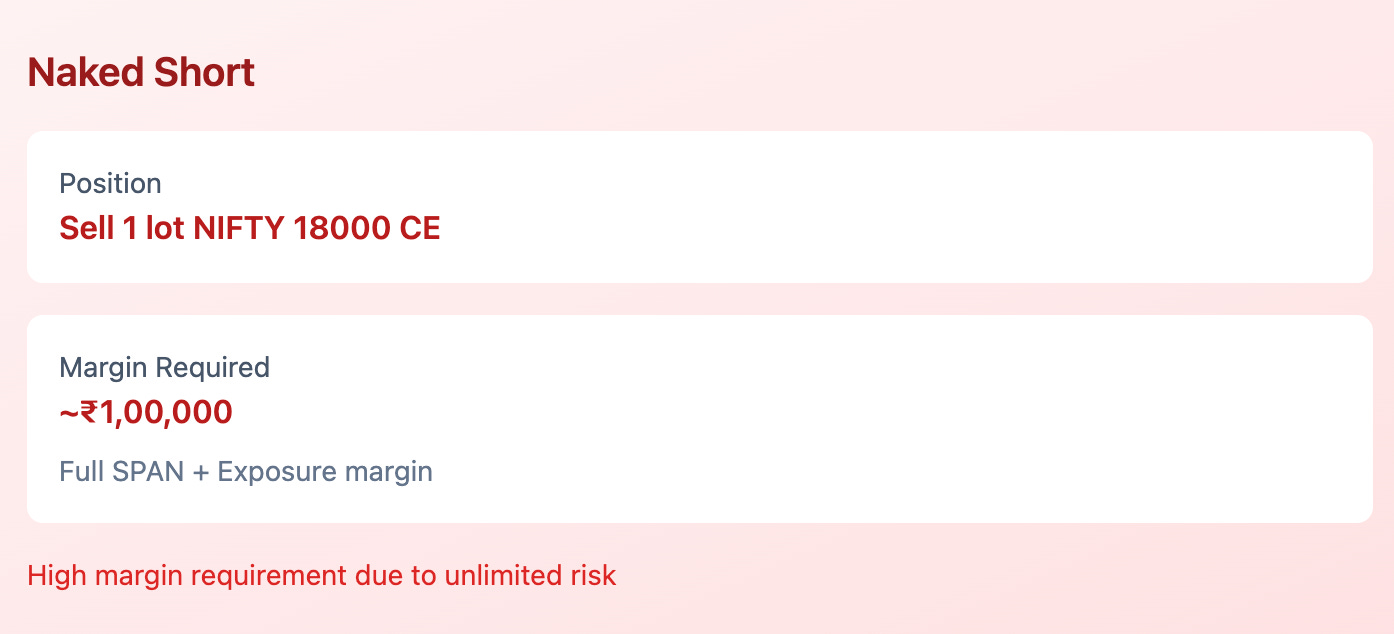

Naked Short Options: If you just sell an option without any hedge, the margin can be quite high. For instance, selling one lot of Nifty call might require, say, around ₹1 lakh (exact amount varies with Nifty level and volatility). This margin consists of SPAN margin (calculated by exchange's risk system for worst-case single-day move) and Exposure margin (an additional buffer, often a percentage of the contract value). The idea is to cover the risk of adverse movement. Short puts similarly require margin (short put risk is if market falls a lot)

Hedged Positions: If you have a hedge, the risk reduces and so do margins. Example: You sell a Nifty 18000 Call but also buy a Nifty 18200 Call (same expiry) as protection. Your maximum loss is limited (it’s a spread). In such cases, the margin requirement is much lower than two separate naked positions. In 2020, SEBI implemented a new framework reducing margin requirements for hedged positions by about 60-70% . This was great news for traders using strategies: “margin requirement reduced for positions which have limited risk ... by almost 70%” . So a spread that might have needed ₹1 lakh before, might only need ₹30k now. However, naked positions still require the same margin as before

Example Numbers: Suppose a naked short Nifty call needs ₹1,00,000 margin. If you pair it with a long call above (limited loss strategy), maybe you only need ₹30,000 now. If you do an Iron Condor (two calls, two puts hedged), margin might be even lower per lot, say ₹20k. These are ballpark figures, actual margin is computed by broker’s backend using NSE’s SPAN software.

SEBI Margin Regulations & Recent Changes:

Upfront Margin & Peak Margin: SEBI now requires 100% upfront collection of margin for all F&O trades. In 2021, the “peak margin” rules were fully implemented. Under these rules, traders must maintain the total required margin throughout the trading day, not just by end of day . If at any point you don’t have sufficient margin, the broker will flag it and you could face a penalty. This killed the old practice of high intraday leverage provided by brokers. Now, even for intraday option selling, you need essentially the same margin as overnight. Translation: If margin for a position is ₹50k, you need that ₹50k before taking the trade; you can’t just have ₹10k and hope to square off quickly (that would violate margin rules).

Margin Benefits for Hedge (Same Account): To get the reduced hedged margin benefit, the positions usually have to be in the same account and entered in correct order. Brokers’ systems are designed to recognize a hedge. For example, if you buy a call first and then sell a call, you immediately get margin benefit. If you sell first and then buy the hedge, you might temporarily need full margin until the hedge is in place (brokers often auto-combine for margin calc, but caution is warranted especially on expiry – more on that in a moment).

Expiry and Margin (special case): One nuance: on expiry day, if you have a hedged position where one leg is expiring, some brokers or exchange might remove the margin benefit toward the end. For example, a calendar spread (short near month, long far month) – on expiry of the near month, that hedge is gone, so just before expiry they might ask full margin or square off. Recently, a circular indicates margin benefit on hedges won’t be allowed on the last day for the expiring leg . So be mindful of expiry handling of hedges.

Lot Size / Contract Value Changes: SEBI mandated that minimum contract size (underlying value * lot size) for index futures/options should be ₹5 lakh historically and recently moving to ₹15 lakh . This led to periodic revisions of lot sizes. For example, Nifty’s lot was reduced from 75 to 50 in 2021 when Nifty was around 15k (to keep value ~7.5 lakh). They plan to increase it to ensure ₹15 lakh value, likely meaning Nifty lot might go back to 75 if Nifty ~20k. BankNifty’s lot has changed multiple times (20, 25, etc.) for similar reasons. This impacts retail traders because the minimum capital to trade one lot changes. (As per an example, if an option is ₹400 and lot increases from 25 to 75, the cost for one lot goes from ₹10k to ₹30k) . So keep updated on lot size changes – it affects your position sizing.

What Does This Mean for a Retail Trader?

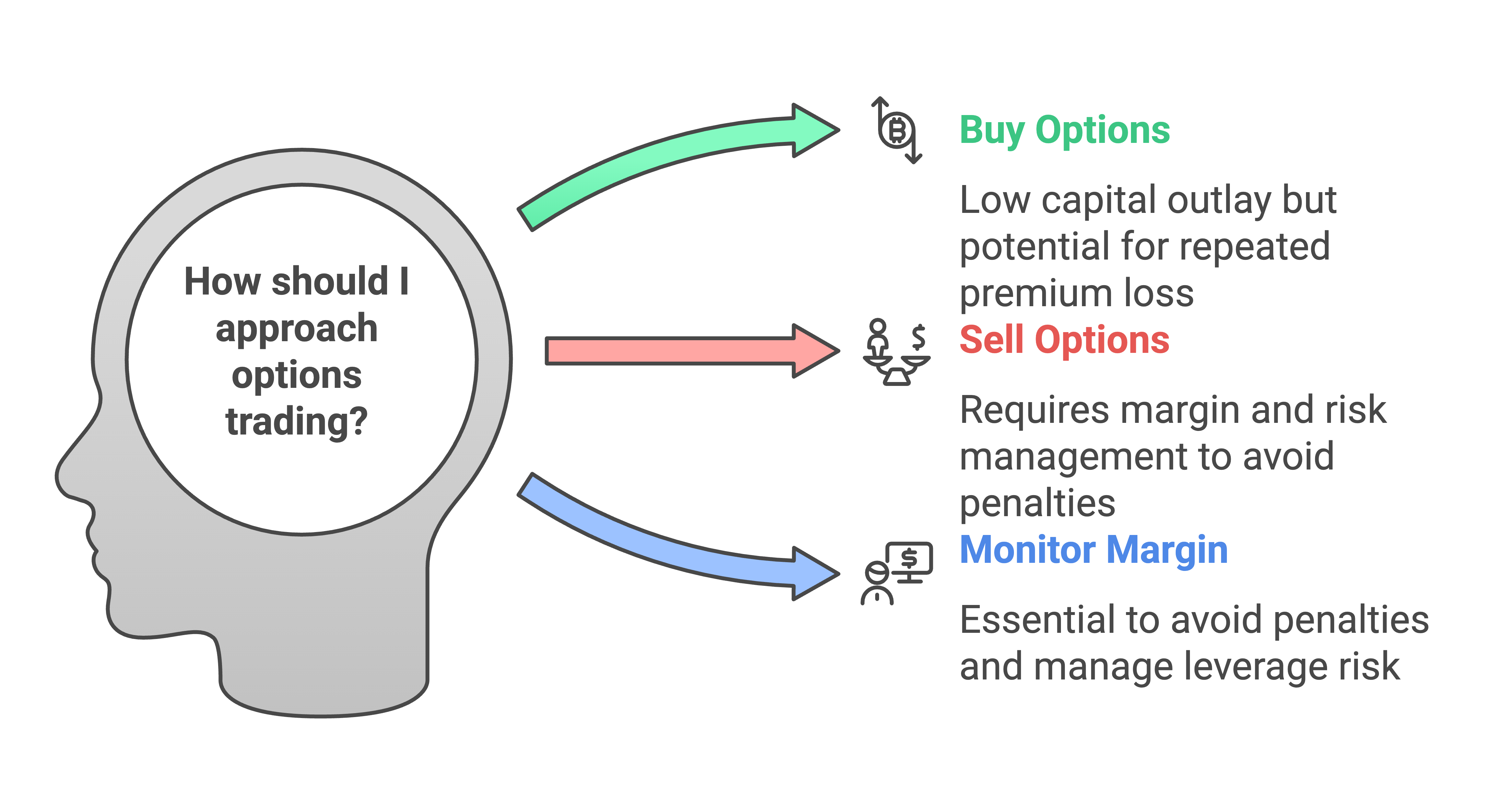

If you buy options, your capital outlay is just the premium. But remember, buying too far OTM might be cheap but low probability – you could lose premium repeatedly. Still, no margin headache there.

If you sell options, ensure you have sufficient margin. Use the SPAN calculator (many brokers provide online) to check margin impact of a trade before executing. If you want to do strategy trades (spreads, iron condors, etc.), understand how the broker grants margin benefit. Usually, the combined position margin is much less than sum of individual legs.

Avoid margin penalties: Always monitor your account, especially in volatile markets. If your sold option goes deep ITM and starts losing money, margin requirement might increase (because risk increases). Brokers will typically send alerts if you’re short. Top up funds or reduce positions to avoid auto-square-off.

Leverage with caution: Options selling can give steady income (from premium decay), but it uses leverage. You might be writing ₹5 lakh of notional exposure with ₹50k margin. If things go south, that ₹50k can turn to loss quickly if you don’t have a hedge or stop.

SEBI’s intent with strict margins is to protect the market from over-leveraged bets that could default. It levels the field (since Sept 2021, all brokers enforce similar margins). Yes, it means you can’t get crazy intraday leverage, but it also prevents a lot of blown-up accounts.

In summary, know the cost of entry:

Buying? Pay premium, no extra margin.

Selling naked? Significant margin – consider strategies to reduce it.

Always adhere to SEBI/Broker margin rules; penalties for shortfall are real (and can be a percentage of shortfall, eating into profits).

Now, let’s talk about who is on the other side of our trades providing liquidity and maintaining these markets – the Market Makers in options trading.