How One Trader Triggered a $1 Trillion Flash Crash — and Changed Market Regulation Forever

On May 6, 2010, nearly $1 trillion was wiped off the U.S. stock market in under 30 minutes.

The culprit?

Not a hedge fund.

Not a rogue AI.

But a single trader — Navinder Singh Sarao, operating out of his parents' home in suburban London.

Sarao didn’t hack the system. He didn’t even break it.

He simply exploited it — using tools available to most traders and one key tactic: spoofing.

But this isn’t a story about how clever he was.

It’s about how unprepared global markets were and how this case reshaped how regulators think about electronic trading — even today.

How It Worked — And Why It Worked So Well

Navinder Singh Sarao didn’t invent some genius algorithm or hack into Wall Street.

He used a tactic called spoofing — placing huge orders in the market with no intention of executing them, only to cancel them once they’d moved the price in his favor.

Here’s how it played out:

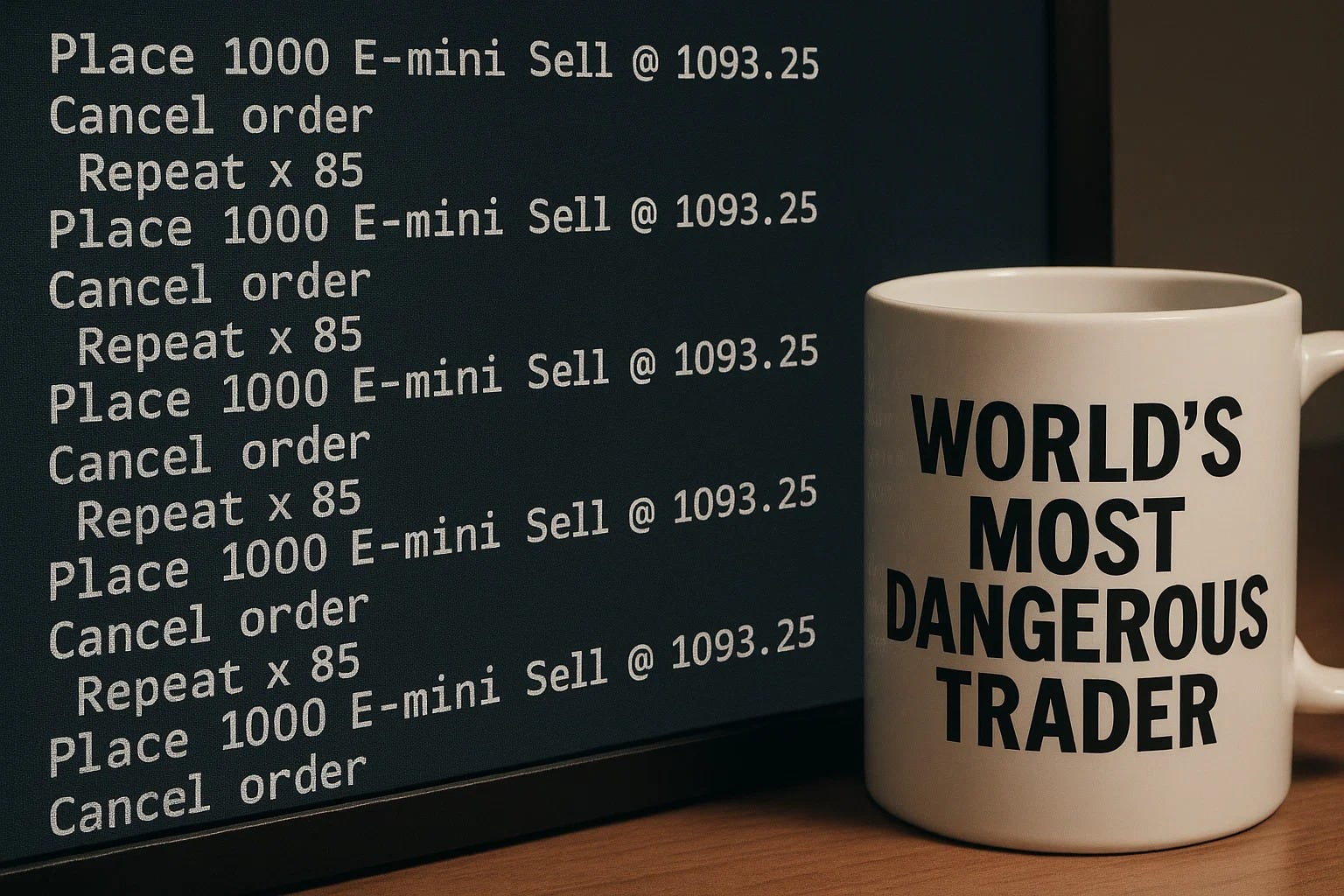

He’d place massive sell orders just above the current price in E-mini S&P 500 futures.

Other traders — bots and humans — would see this flood of selling and assume a drop was coming.

Prices would fall. Sarao would buy at the dip.

Then he’d cancel his fake orders and sell into the rebound — all within seconds.

This wasn’t a one-off stunt.

Sarao ran this play thousands of times between 2009 and 2014, aided by custom-modified software that let him flood the order book and cancel positions faster than most traders could blink.

The scariest part? It worked for years — and no one noticed.

He wasn’t bigger than the market. He just understood how little it took to tip it.

The Flash Crash: When Everything Broke in 30 Minutes

On May 6, 2010, the Dow Jones dropped nearly 1,000 points in under 30 minutes, briefly erasing almost $1 trillion in market value before rebounding just as quickly.

It was one of the most chaotic trading days in modern history.

And while there were many contributing factors — from algorithmic trading loops to thin liquidity — Sarao’s spoof orders played a measurable role in the chain reaction.

That day, he entered more than 85 large spoof orders, at times representing over 20% of all visible sell orders in the E-mini S&P 500 futures market.

The result?

Algorithms saw heavy selling pressure and panicked.

Market makers pulled liquidity.

Prices free-fell, triggering more sell orders.

And the entire system briefly spiraled — until human intervention and circuit breakers kicked in.

The scariest part? One trader’s fake orders helped accelerate one of the largest intraday collapses ever.

Not because he broke the market.

Because he revealed how easily it could be nudged off balance.

Before the Truth: Theories, Finger-Pointing, and Total Confusion

When the market dropped nearly 1,000 points in minutes on May 6, 2010, no one had a clear explanation.

Within hours, regulators, exchanges, and the media were scrambling to piece together what had just happened. And the theories came fast:

Fat Finger Error: Early headlines pointed to a trader who may have accidentally entered a massive sell order — like adding an extra zero to a Procter & Gamble trade. It was catchy, but it didn’t hold up. The timing didn’t match, and CME safeguards would’ve blocked it.

High-Frequency Trading Meltdown: Some blamed HFT firms for flooding the market with cancelable orders or abandoning it when volatility spiked. While HFTs weren’t blamed outright, regulators later confirmed they did worsen the crash by selling aggressively and drying up liquidity.

Quote Stuffing & Glitches: Others suspected technical issues — delayed quotes, overloaded exchanges, and bad data flowing through systems. Some firms were seeing delayed prices while others had real-time access. It created a fog that made panic selling worse.

One Giant Trade?: Attention eventually turned to a large institutional order 75,000 E-mini S&P contracts sold by Waddell & Reed using a basic volume-based algo. This wasn’t illegal or unusual, but it became a spark in a dry forest.

Even after the SEC and CFTC released their joint report, many critics pushed back. Some said regulators were oversimplifying. Others argued they were under-equipped to investigate in real time.

The reality was — and still is — that no single factor caused the Flash Crash.

It was a breakdown across layers: structure, tech, behavior, and oversight.

That’s what made Sarao’s later arrest so stunning: it wasn’t just that he spoofed the market — it was that he spoofed a system that was already on the edge.

What Changed After: Regulation Woke Up

Sarao didn’t just profit from spoofing.

He unintentionally exposed just how vulnerable modern markets had become — especially in an era dominated by speed, automation, and algorithms chasing each other’s shadows.

And regulators took notice.

Here’s what changed in the years that followed:

Spoofing Became a Crime (Officially)

Before the Flash Crash, spoofing existed in a regulatory grey zone.

After it, the Dodd-Frank Act (2010) formally defined spoofing as illegal market manipulation. That meant clearer rules — and real consequences — for using fake orders to move price.

Better Surveillance, Smarter Detection

Market watchdogs like the CFTC and SEC invested heavily in tech that could analyze millions of orders in milliseconds.

Instead of just looking at trades, they started analyzing intent — patterns of placing and cancelling orders to manipulate sentiment.

Circuit Breakers and Liquidity Protections

The Flash Crash triggered a rethink on market structure.

New circuit breakers were introduced to pause trading during extreme volatility, giving markets (and humans) time to breathe.

Global Coordination Improved

Regulators across jurisdictions realized if one trader in London can shake Wall Street, regulation can’t be local. International cooperation on cross-border cases became tighter — and faster.

Sarao’s case showed that the threat wasn’t just rogue traders — it was infrastructure gaps.

And fixing them meant rebuilding trust in the system.

What Traders Should Actually Take From This

It’s easy to frame stories like this around “one genius trader who outsmarted the system.”

But that misses the point.

Navinder Singh Sarao didn’t win.

He exploited a weakness — and in doing so, exposed how fragile that system really was.

The real lesson isn’t in the spoofing. It’s in what came next.

Markets learned. Regulators adapted. Systems evolved.

Because the cost of not evolving was a trillion-dollar breakdown — and a loss of trust.

As traders, we don’t control the system — but we operate inside it.

And that means understanding how infrastructure, rules, and transparency shape what we trade and how we manage risk.