Market Minute | Weekly Wrap-up

🚀Nifty50: Sharp bounce from 25.7K, Muthoot Finance gains ~10%; WPI Inflation falls to -1.21% & full weekly wrap inside!

Nifty 25,910.05 ▲ +0.12%

Sensex 84,562.78 ▲ +0.10%

Bank Nifty 58,517.55 ▲ +0.23%

How did the Markets move today? A volatile start, A strong finish!

Ever wondered how quickly sentiment can flip within a single session? Today was a perfect example. The day began on the back foot, with Nifty50 slipping toward 25,740, but the mood changed dramatically in the final hour. A sharp recovery helped the index finish at 25,910, while the Sensex closed 84 points higher. Bank Nifty stayed firmly aligned with the benchmark moves, ending at 58,518, inching closer to its all-time high.

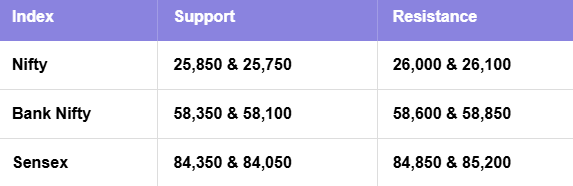

What’s the market hinting at? If Nifty holds above 25,740, the upside remains intact, and a clear move above 26,000 could unlock 26,100. For the Sensex, watch 84,850 and 85,200 as resistance zones. And Bank Nifty needs a breakout above 58,615 to print fresh highs, with nearby supports at 58,350–58,250 now turning into a polarity zone.

Sectoral & Stock Action!

If there’s one question worth asking today, it’s this: Which pockets really drove the rebound? The answer lies in the sectoral divergence.

PSU Banks led the show, followed by Pharma, FMCG, and Financial Services, all contributing to the market’s upward push.

On the other hand, IT, Metals, and Auto remained muted, bucking the broader positive trend.

In the midcap universe, action was just as vibrant. Samvardhana Motherson, Muthoot Finance, Vodafone Idea, and NALCO clocked impressive gains, while select names like GMDC fell after weak earnings. Broader market indices were mixed, Midcap 100 stayed flat, while Smallcap 100 edged up 0.38%.

The Bigger Picture: Strongest week in 5 months as Markets snap losing streak!

Beyond the daily moves, the real story is the weekly performance. After 2 straight weeks of weakness, the markets staged their best weekly gain in 5 months. Nifty, Sensex, and the Midcap index each rose close to 1.6%, while Bank Nifty added 1.11%.

All sectoral indices closed the week in the green, with the Defence sector stealing the spotlight, up 4.4%, making it the biggest outperformer of the week. A remarkable 35 Nifty stocks ended higher this week, including strong names like Asian Paints, Adani Enterprises, InterGlobe Aviation, and HCLTech.

The takeaway? Not only did the market recover, but it also showed breadth, conviction, and leadership across segments, a combination that often fuels sustained momentum.

NIFTY50: Top Gainers

Zomato ▲ +2.02%

BEL ▲ +1.68%

Trent ▲ +1.50%

NIFTY50: Top Losers

Infosys ▼ -2.53%

Eicher Motors ▼ -2.33%

Tata Motors ▼ -1.70%

Key levels to watch for November 17, 2025

OI Insights

Put writing at 25,700 (37.9L) shows strong defense from traders, marking it as a solid support zone. On the other hand, heavy call additions at 26,000 (57.75L) highlight selling pressure near that resistance level. The PCR-OI is at 0.8.

What does this mean? The setup suggests traders expect Nifty to stay above 25,700 and potentially push toward 26,000 or higher, keeping the overall sentiment tilted upward.

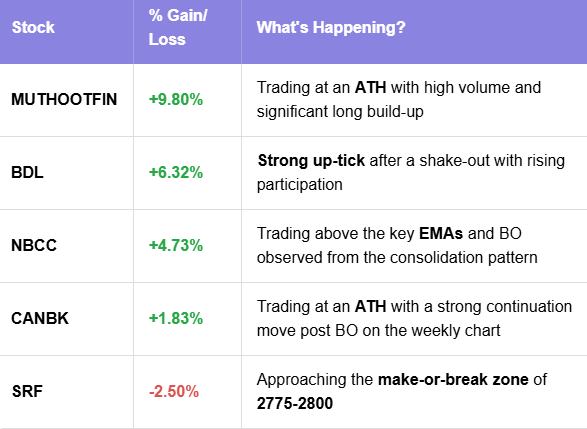

Today’s buzzing stocks at a glance

News you can use

October WPI inflation falls to -1.21% vs 0.13%.

Tata Motors PV reports 22-fold profit surge on ₹82,616 crore demerger gain; core business posts ₹6,368 crore loss.

MRF Q2 profit rises 12% YoY to ₹525.64 crore; announces ₹3 dividend.

KPI Green Energy signs ₹696 crore contract with SJVN for 200 MW solar project in Gujarat.

BASF India Q2 profit declines 16.4% YoY to ₹107 crore.

BEL secured fresh orders worth ₹871 crore since last update.

ITC block deal: 5.2 crore shares (0.4% equity) worth ₹2,074.5 crore change hands at ₹402 per share.

Chart of the day: GRSE

Spotted: Pennant

Structure: Forms after a sharp move followed by a brief, converging consolidation resembling a small triangle.

Validation: BO above the upper trendline on strong volume confirms continuation.

Trading Insight: A continuation pattern signaling pause before the next leg up; enter on BO with volume support.

That’s a wrap for today’s action-packed session! We’ll be back in your inbox on November 17, 2025, with more sharp insights, fresh trends, and signals from the markets. Until then, have a great weekend!