A big structural change is coming to the derivatives market. Both NSE and BSE have revised the expiry days for index and stock derivative contracts.

Yes, you read that right, the expiry, which has always been on Thursday, will now shift to Tuesday from August 29,2025.

When was this announced?

Announced: June 23, 2025 (NSE Circular)

Let’s break it down:

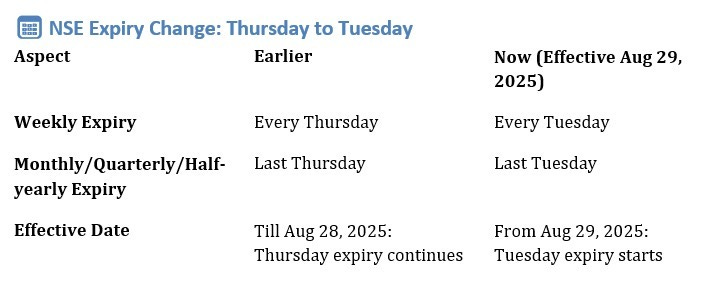

NSE

1. Weekly expiry (NIFTY): Shifting from Thursday to Tuesday.

2. Monthly / Quarterly / Half-yearly (Only for NIFTY & BANK NIFTY): Shifting from last Thursday to last Tuesday.

3. Monthly expiry only: FINNIFTY, MIDCPNIFTY, NIFTYNXT50 & F&O stocks.

The first Tuesday weekly expiry for Nifty50: September 02,2025.

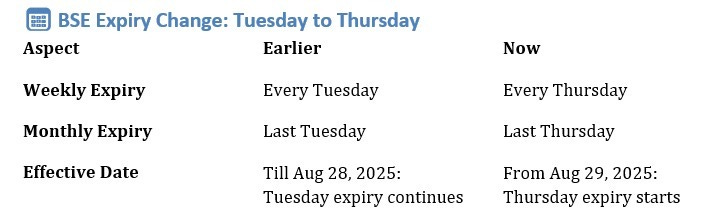

BSE

1. Weekly expiry (Sensex): Shifting from Tuesday to Thursday.

2. Monthly expiry (Sensex, Bankex, Sensex 50): Shifting from last Tuesday to last Thursday.

3. Quarterly / Half-yearly (Sensex): Same shift from Tuesday to Thursday.

The first Thursday weekly expiry for Sensex: September 04,2025.

Important Points for Traders:

1. Effective from September 2, 2025: All new contracts will reflect revised expiry days.

2. Existing contracts (till August 29, 2025 EOD): Will follow the old expiry schedule.

3. Holiday adjustments: If revised expiry day is a holiday, expiry moves automatically.

The potential impact?

Why does this matter? Volumes tell the story.

Now, while both NSE and BSE technically have a full week between expiries, the difference lies in where the liquidity builds up.

For NSE (Tuesday expiry), the effective runway is Friday, Monday, and Tuesday. These 3 sessions see heavy volumes, giving traders more breathing room to speculate and adjust positions. NSE already dominates this space, clocking ₹2.5–3 lakh crore in daily derivatives turnover on expiries.

For BSE (Thursday expiry), the runway shrinks to just Wednesday and Thursday. Even though Monday and Tuesday exist in the cycle, liquidity naturally gravitates to NSE. That leaves BSE’s expiry action squeezed into fewer days, with volumes averaging a much smaller ₹10–15k crore.

Analysts expect this shift to tilt the balance. Goldman Sachs projects BSE’s market share in index options could slip from ~24% to ~21%, while NSE may reclaim up to 5% more market share in turnover.