Volatility is the heartbeat of options pricing. It’s so crucial that an option’s price can be high or low even if the underlying price is the same, just based on volatility expectations. Let’s break down what volatility means for options, focusing on Implied Volatility (IV), and concepts like IV crush especially in the Indian market context (think Budget Day, earnings, etc.).

What is Volatility?

In simple terms, volatility is a measure of how much an asset’s price swings or is expected to swing. There are two common references:

Historical (Realized) Volatility: How much the underlying’s price has actually been fluctuating (e.g., over the last 1 month, Nifty’s volatility was X% per annum).

Implied Volatility (IV): The volatility level implied by the current option prices, i.e., what the market expects for the future. IV is essentially backed out from option prices using models like Black-Scholes. If options are expensive, IV is high; if they’re cheap, IV is low.

In India, we have a handy index for overall market volatility: India VIX – it’s derived from NIFTY options and indicates the implied volatility of the market. A high VIX means option premiums are high (market expecting big moves), a low VIX means complacency (expecting calmer moves).

Impact of Volatility on Premiums:

Higher volatility makes options more expensive, all else equal. Why? Because if an underlying swings wildly, any option has a greater chance to end up ITM by expiry. So sellers demand more premium to compensate for that risk, and buyers are willing to pay more for the greater opportunity. Conversely, in a quiet market, options cheapen.

This is where Vega (from Greeks) comes in – it measures how much the premium changes with volatility. But let’s focus on practical aspects:

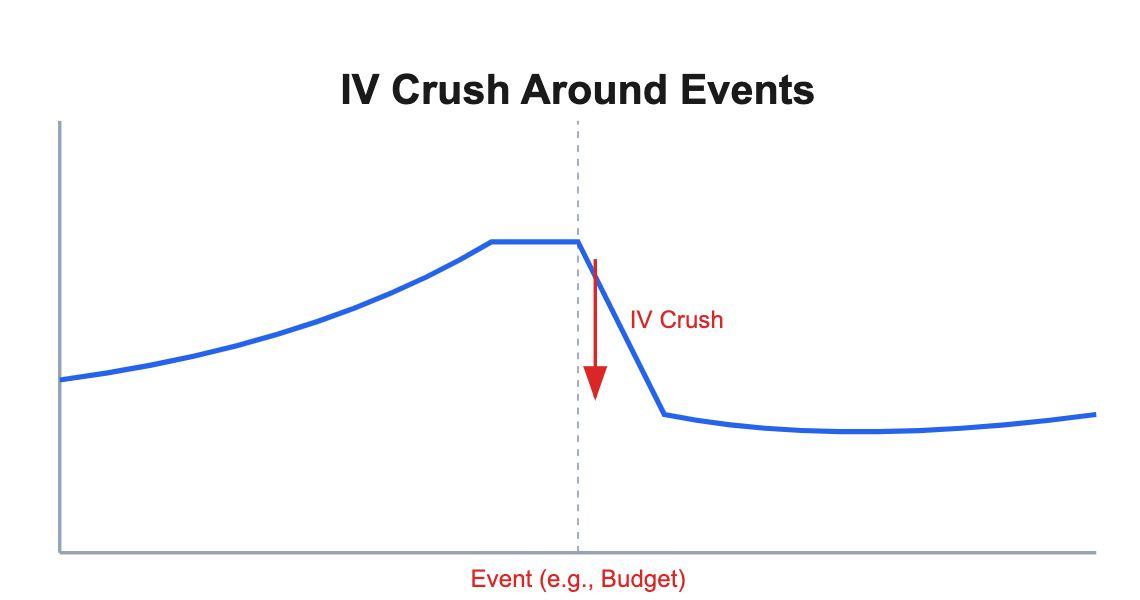

If a stock or index’s volatility is expected to increase (perhaps due to an upcoming event), the implied volatility in options will rise before the event. This causes premiums to go up even if the underlying price hasn’t moved yet.

After the event, volatility usually crashes (often called IV crush) because uncertainty is resolved. Options then become cheaper

Real-World Example – Budget Day IV:

In India, the Union Budget announcement is a major event yearly. Typically, in the days leading up to the Budget, the implied volatility of index options rises, pumping up option premiums. A news article noted: "A common trend observed is that the Implied Volatility (IV) of Options rises in the days leading up to the Budget but subsequently declines sharply during the speech." (Budget day trading strategy: What should Nifty traders do on D-Day? - The Economic Times). Indeed, many traders have seen that right after the Budget speech (once key info is out), option prices drop sharply due to IV crush, even if Nifty doesn’t move much net. If you bought a straddle (both call and put) just before the budget, you needed a huge move to profit, because the post-budget IV crash would deflate the premiums. Sellers of options often benefit in these scenarios by capturing high premium and then IV collapses (as long as the market move isn’t beyond what the premium covered

Other IV Event Examples:

Corporate Earnings (for stocks): If you trade stock options, say Reliance or TCS, you’ll see IV rise before earnings results, and fall right after results are out. Options are priciest just before the event.

Elections, RBI policy, global events: Any scheduled event that could cause uncertainty (e.g., election outcome, central bank meeting, court verdict for a company) will have options price in extra volatility.

Sudden Market Turmoil: If something unexpected happens (say a global market crash or a pandemic breakout), IV can shoot up suddenly – options get very expensive as everyone rushes for protection (puts) or speculation, and market makers widen their volatility assumptions.

IV vs. Direction:

It’s crucial to separate volatility from direction. You might be right about an index staying flat, but if you bought options during high IV, you could still lose money when IV drops. Conversely, you might be wrong about direction but still profit if you sold options and IV collapses (the options lose value due to volatility drop more than the underlying move). Volatility trading (vega trading) is a whole dimension beyond just up/down bets (delta trading).

Implied vs Realized:

Sometimes implied volatility is higher than what actual volatility turns out to be (in which case option sellers generally make money, as they sold “expensive” volatility). If implied is too low and actual moves end up bigger, option buyers profit (volatility was “cheap”). Traders often compare current IV to historical volatility or to its own past levels to gauge if options are relatively cheap or expensive.

Volatility Skew/Smile:

In many markets, not all strikes have the same IV. For index options in particular, often OTM puts have higher IV than OTM calls. This is due to demand for crash protection – investors bid up put prices. The shape of IV across strikes is called the volatility skew or smile. It’s advanced, but just be aware: if you see far OTM puts costing more than equidistant OTM calls, that’s normal in equity indices – the skew.

India VIX and Market Mood:

India VIX (vol index) tends to inversely correlate with Nifty. When markets fall (panic), VIX spikes; when markets rise steadily, VIX falls. Traders watch VIX for sentiment. If VIX is extremely low, options are cheap but there might be complacency (could precede a big move). If VIX is extremely high, options are pricey (maybe too much fear – could be a time for selling premium if one expects mean reversion).

Practical Tip:

Before putting on an options trade, check the IV level of that option or the VIX for indices. Ask, is a big event coming? Are these options relatively expensive or cheap historically? For example, selling options just before an event (to capture high IV) is tempting, but be cautious: you need to be confident the event won’t produce a move larger than the premium collected (or have hedges in place). Buying options when IV is extremely high means you not only need to be right on direction, but also on timing (the move has to outrun the volatility collapse).

In summary, volatility is a key ingredient in the option pricing recipe (the others being underlying price, strike, time, interest, etc.). Mastering options means appreciating the volatility dimension. Many options traders say “you trade volatility, not price.” Now, armed with knowledge of Greeks and volatility, let’s get practical: how do you actually read an option chain and extract useful info for Indian markets?